The Federal Fiscal Mismatch Architecture

The Federal Fiscal Mismatch Architecture

Source: The Hindu

Subject: Federalism

Why in News?

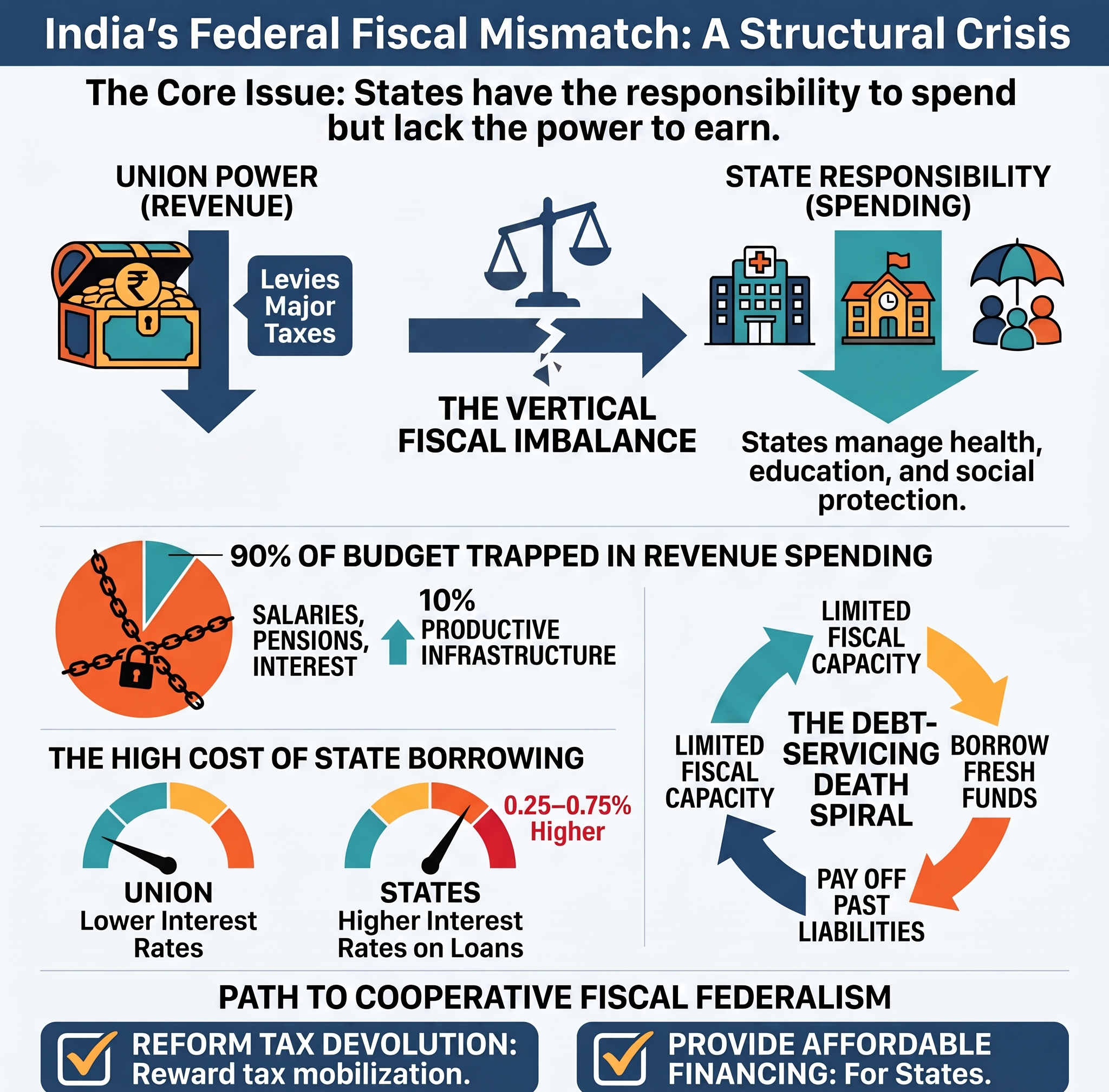

Economist Jayan Jose Thomas has argued that the rising debt burden of Indian States reflects a structural imbalance in India's fiscal federalism, where States bear greater expenditure responsibilities despite having limited revenue-raising powers.

What is the Federal Fiscal Mismatch Architecture?

India's fiscal federal structure creates a vertical fiscal imbalance:

- The Union Government has greater powers to levy and collect major taxes.

- State Governments are responsible for a larger share of public expenditure on:

- Health

- Education

- Agriculture

- Irrigation

- Welfare and social protection

- As expenditure often exceeds available revenue, States increasingly depend on market borrowings through State Development Loans (SDLs).

Key Indicators of Fiscal Stress

Tax Devolution Gap

- Kerala's per capita own tax revenue is 1.5 times the all-India average.

- However, its share in Union tax devolution was only 1.92%, despite accounting for 2.6% of India's population (2023–24).

Revenue vs Capital Expenditure

- Nearly 90% of Kerala's expenditure is devoted to revenue expenditure.

- Only about 10% is available for capital expenditure, limiting future productive investment.

High Committed Expenditure

Kerala's budget is largely pre-committed:

- Salaries: 20%

- Pensions: 15.3%

- Interest payments: 16.5%

This leaves limited fiscal space for infrastructure and development.

Low Credit-Deposit (CD) Ratio

- Kerala's CD ratio: 66%

- National average: 76%

- Maharashtra and Tamil Nadu: Above 100%

This indicates substantial domestic savings are not being effectively channelled into productive investment.

High Cost of Borrowing

- States borrow through State Development Loans (SDLs).

- Interest rate: 6.5–7.5%

- Around 0.25–0.75 percentage points higher than Union Government borrowing costs.

Major Structural Challenges

- Limited fiscal capacity restricts investment in higher education, research, innovation and modern infrastructure.

- High revenue expenditure cannot be sharply reduced without affecting health, education and welfare outcomes.

- Rising debt servicing creates a cycle where fresh borrowings finance past liabilities instead of productive assets.

- Visible private prosperity alongside weak public finances widens regional inequalities.

- Inadequate investment opportunities contribute to brain drain, especially from highly educated States like Kerala.

China's Local Government Model

China follows a decentralised investment-led development model where local governments finance infrastructure through:

- Local Government Bonds (LGBs)

- Land sales

- Local Government Financing Vehicles (LGFVs)

Advantages

- Borrowing cost around 2%, much lower than Indian SDLs.

- Large domestic savings are efficiently channelled into infrastructure and industrial development.

- Central planning ensures coordinated investment across provinces.

Way Forward

- Reform tax devolution formulas to better reward States with stronger own-tax mobilisation.

- Improve States' access to domestic savings through innovative financing mechanisms.

- Reduce borrowing costs by strengthening the SDL framework and providing greater Union support.

- Gradually increase capital expenditure while preserving essential social sector spending.

- Strengthen cooperative fiscal federalism through predictable transfers and greater fiscal autonomy.

- Develop portable welfare systems to support labour mobility across States.

Conclusion

India's rising State debt is fundamentally a consequence of structural fiscal imbalance rather than fiscal indiscipline. Empowering States with greater fiscal autonomy, affordable financing and a more balanced revenue-sharing framework is essential for sustaining inclusive growth and strengthening cooperative federalism.

Final Takeaway

India's fiscal federalism must evolve from a system where States carry most development responsibilities to one where they also possess adequate fiscal capacity. Sustainable State finances require not only prudent borrowing but also fair devolution, lower borrowing costs and greater investment in long-term productive assets.